Is Novartis Desperate or Just Insane? A $12 Billion Bet on a Biotech Prayer

So, Novartis just threw $12 billion at a biotech company called Avidity Biosciences. Let that sink in. Twelve. Billion. Dollars. For a company that, as of today, sells exactly zero approved drugs. They paid a 46% premium over the `avidity stock` price, which is the kind of move you make in a poker game when you're either holding a royal flush or you're sweating bullets and trying to bluff your way out of a terrible hand. Novartis To Acquire Avidity Biosciences In $12 Bln Deal

I'm leaning towards the latter.

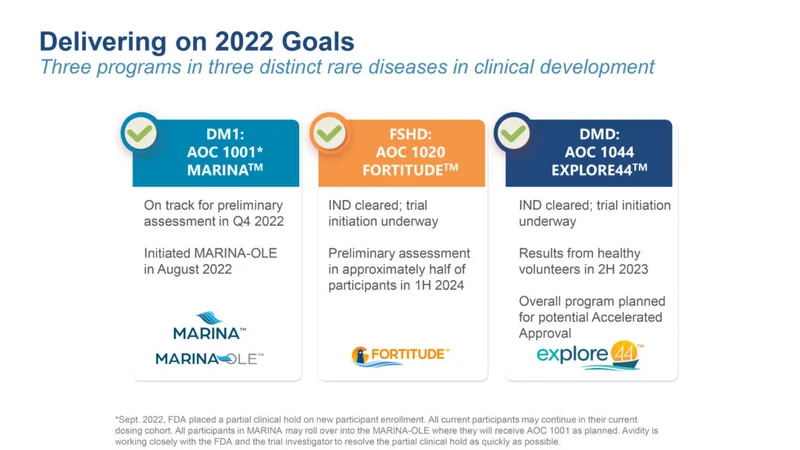

Let’s be real. When a pharma giant like Novartis shells out that kind of cash, it’s not just a vote of confidence. It’s a scream of desperation. Their pipeline is getting old, patents are expiring, and they need a shiny new toy to show Wall Street. And `Avidity Biosciences Inc` is one hell of a shiny toy. They’re working on RNA drugs, the current belle of the biotech ball, targeting nasty neuromuscular diseases like Duchenne muscular dystrophy.

This is a bold move. No, 'bold' is what you say in a press release—this is a white-knuckle, bet-the-company gamble. They're not just buying a product; they're buying a promise. A promise that Avidity’s fancy "AOC" platform can deliver RNA therapies to muscle tissue, something that's been notoriously difficult. It's like betting on a theoretical rocket engine that’s only ever been fired on a computer simulation. Will it get you to Mars, or will it blow up on the launchpad? Who knows! But for $12 billion, you'd hope for at least a decent blueprint.

The PR machine, offcourse, is already in overdrive. Novartis CEO Vas Narasimhan is talking about their “commitment to delivering innovative, targeted and potentially first-in-class medicines.” It's the standard corporate script, so polished and meaningless it could have been generated by an algorithm. Here’s the Nate Ryder translation: “We are terrified of becoming irrelevant, and this company has three lottery tickets in late-stage trials that might pay off before our investors revolt. Please clap.”

This ain't just about science; it's about market panic. The whole `rna stock` sector is hot right now, and Novartis is paying top dollar to get in the game before a competitor like `Dyne Therapeutics` corners the market. But what are they actually getting for their money? A trio of drugs that are still waiting for the FDA’s blessing. Avidity says they’re on track for submissions, with the first one coming in early 2026. That’s a lot of time for things to go spectacularly wrong. What if the data isn't as clean as they hope? What if the FDA finds an issue? For $12 billion, you’re not just buying potential success; you’re buying a mountain of risk.

The Shell Game with the "SpinCo"

Now, here’s where the story gets really interesting—and a little shady. As part of this glorious union, Avidity is carving out its early-stage cardiology programs and spinning them off into a new, publicly traded company. This little entity, creatively dubbed "SpinCo" for now, gets $270 million in cash and will be run by Avidity’s current leadership team.

Give me a break.

This isn't a merger; it's a corporate dissection. Novartis is acting like a picky eater, carefully separating the peas from the mashed potatoes on its plate. They want the juicy neuroscience assets but clearly have no interest in the cardiology stuff. So, they let Avidity’s execs take their pet projects, a pile of cash, and go start a new life. Avidity shareholders get a tiny sliver of this new company, but let's be honest, the real prize for them is the fat 46% premium Novartis is paying for their `avidity biosciences stock`. I can practically hear the champagne corks popping in San Diego.

It feels like a perfectly legal, expertly crafted way to gut a company for its most valuable parts while letting the old guard parachute out with a golden handshake. Why not just acquire the whole damn thing? What does Novartis know about those cardiology programs that makes them so eager to avoid them? Are they duds? Is this a way to sweep potential liabilities under a different corporate rug? We’re left to guess, because transparency is a four-letter word in deals like this.

It all reminds me of trying to cancel my cable subscription. They transfer you five times, offer you a bundle you don’t want, and make the whole process so convoluted that you just give up. This SpinCo maneuver feels like that. It’s complexity for the sake of complexity, designed to obscure a simple transaction: Novartis is buying a few specific lottery tickets, and everyone involved is getting a nice payday before we even know if those tickets are winners. They’re paying a massive premium for a company with zero approved drugs and a promise of maybe, just maybe, hitting it big...

This whole saga is a perfect snapshot of modern pharma. Innovation isn't happening in-house anymore. It's too slow, too risky. The new model is to let hundreds of smaller, nimbler biotechs like Avidity take the early risks, burn through venture capital, and then, if one of them gets remotely close to a breakthrough, a giant like Novartis swoops in with an offer they can't refuse. They aren't building the future; they're just buying it, piece by expensive piece.

Another Spin of the Pharma Roulette Wheel

At the end of the day, don't let the talk of "pioneering platforms" and "devastating diseases" fool you. This is a financial transaction, plain and simple. It's a calculated risk by a massive corporation desperate for growth, and it's a massive payday for Avidity's founders and investors. The patients? They're just a talking point in the press release, the emotional justification for a multi-billion-dollar bet placed at the high-stakes table of biotech M&A. Maybe the drugs will work and change lives. I hope they do. But that outcome feels almost incidental to the deal itself. This was about securing assets, placating Wall Street, and keeping the `Novartis stock` ticker pointing up. The rest is just marketing.